March 5, 2020 - Squared Away Blog

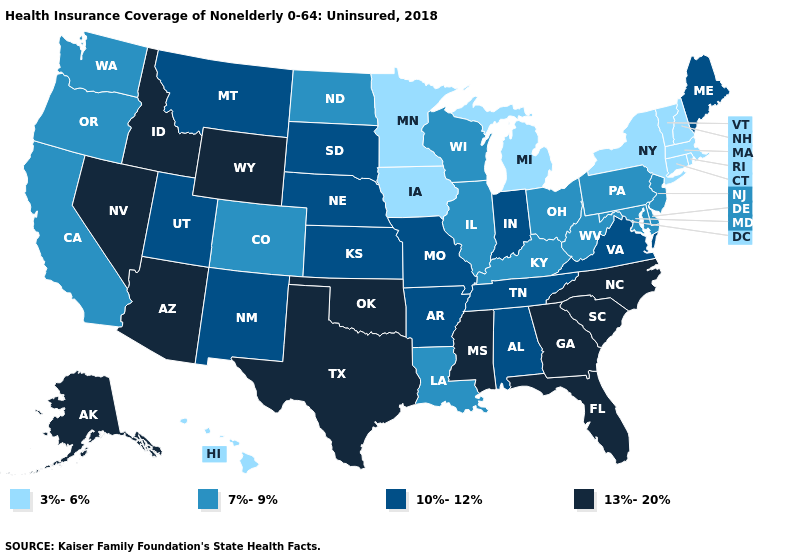

A decade after the passage of the Affordable Care Act, about one out of every five Texans under age 65 still do not have health insurance. Georgia, Oklahoma and Florida are close behind.

The contrast with Hawaii, Minnesota, Michigan, and New Hampshire is stark – only about one in 20 of their residents lacked insurance in 2018, the most recent year of available data, according to the Kaiser Family Foundation’s annual roundup of insurance coverage in the 50 states.

Despite this glaring disparity, the share of Americans lacking coverage has dropped dramatically across the board, including in Texas. Texas’ uninsured rate fell from 26 percent in 2010 to 20% percent in 2018. This translates to nearly 5 million more people with health insurance. (Large populations of undocumented immigrants in states like Texas can push up the uninsured rate.)

States that had fairly broad coverage even prior to the Affordable Care Act’s (ACA) 2010 passage didn’t have as far to fall. For example, Connecticut’s uninsured rate is 6 percent, down from 10 percent in 2010.

One upshot of these two trends is that the disparity between the high- and low-coverage states has shrunk. Certainly, the strong job market gets credit for reducing the ranks of the uninsured. But millions of Americans who don’t have employer insurance have either purchased a policy on the insurance exchanges or gained coverage when their state expanded Medicaid to more low-income residents under the ACA.

For example, just two years after Louisiana’s 2016 Medicaid expansion, the uninsured rate had fallen from 12 percent to 9 percent.

But the initial benefits of the ACA seem to have played out. The U.S. uninsured rate increased slightly, from 10 percent to 10.4 percent between 2016 and 2018.

The share of people who are underinsured is also rising, the Commonwealth Fund found in a recent analysis.

One big source of underinsurance is rising deductibles in employer health insurance. People are counted as under-insured if their out-of-pocket costs, excluding premiums, exceeds 10 percent of their income, making it difficult to pay for medical care out of their own pockets.

Middle-income people who purchase ACA coverage are also underinsured. The deductibles on the standard silver plans are very high – several thousand dollars – in many states. Yet middle-income workers may earn too much to qualify for the generous tax subsidies available to low-income workers under the program.

Squared Away writer Kim Blanton invites you to follow us on Twitter @SquaredAwayBC. To stay current on our blog, please join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here. This blog is supported by the Center for Retirement Research at Boston College.